The 15th edition of the “E-commerce in Italy” conference has been held online on May 7, 2021.

2020 has created a rising demand from millions of people that had never before tried online trading and has, above all, brought about a shift in investment by many businesses that now see online sales as a way to navigate their way through the current crisis.

For this reason, 2021 will be the year of major moves in the e-commerce market, with operations aimed at consolidation and an internal shift within businesses whereby online trading will no longer be relegated to being an area of research and development but will instead become an essential part of the businesses.

Download the research

Download

Like a pot on the stove about to boil, just needing a tap on its side to start, the lockdown was the tipping point of Italian e-commerce.

Many sectors have suffered, mainly tourism which was always the driver of Italian online commerce. That is why 2020 has been a transition year. Those who were able to seize the moment have seen a significant growth in turnover (e.g., Food, because of closed restaurants) or profits (e.g., car insurance, because of the absence of accidents). For others it was a moment of survival (e.g., Tourism).

That is why the e-commerce sector’s end of year result has remained, for the first time ever in Italian history, basically the same as the previous year.

But 2020 really brought a maturation of e-commerce, it became truly mainstream. Millions of Italians have discovered the possibility of buying online and they will not forget it, even for the sectors that have suffered in recent months. That is why today e-commerce has become fundamental to the strategy of every production or distribution group in Italy.

When a sector goes through a maturation change there are many side effects. One of these is the takeovers made by companies that want to consolidate their position or that want to make up for lost time. Another changing factor are infrastructures that are becoming critical to excel in the sector. For this reason, pressures are also emerging to define the game table. For example, for some years now, network neutrality is being discussed: equal access for all companies to the same quality and speed of Network (e.g., especially for streaming companies in the United States). Today, in Italy, we must also question other infrastructures such as shipping neutrality. The presence of large operators is in fact shifting attention and quality of service towards those who contractualize very challenging SLAs (Service Level Agreements) to the detriment of small Italian e-commerce operators with much less contractual force.

For this and other reasons linked to the economies of scale of the large international giants, new forms of aggregations are being created between companies which, through federations of micro-enterprises, are increasingly positioning as valid competitors (at least in perspective).

In Italy there are about 10 thousand companies in the logistics sector, with 85 billion turnover in 2019, 9% of the national GDP. About 90% of them are micro or small businesses, with less than 9 employees and little opportunity to invest heavily in digital transformation1.

Despite the growth in e-commerce volumes, and therefore of shipments (+55% in June 2020 compared to 20192), the logistics sector had a sharp decline, especially at the beginning of the lockdown, -35% , due to the halting of industrial shipments3.

Shipments generated by e-commerce have increased +103% during lockdown and 68.5% after lockdown, showing that the trend will continue4: Throughout 2020, supply chain and logistics operators had to deal with large volumes of work related to B2C deliveries and growing expectations from consumers, also contending with the incremental security measures linked to the Pandemic. Operators such as Asendia Italia, observed higher traffic of small packages (+120% compared to the previous year) and consequent growth in turnover linked to the service.

Moreover, Italy was the first European country to face the Pandemic, therefore, it acted as the test in managing the organisational structure relating to e-commerce.

Top logistics competitors have seen their activity continue to grow: In 2020 with this in mind, Amazon created 120,000 new jobs in construction and “Amazon Logistics”, while UPS opened a new logistics point in Tuscany. At the end of last year, even Poste developed a new “MaxiHub” in Rome, a highly automated logistics facility, capable of handling on average 140,000 parcels per day (the hub in Milan will be launched in spring 2021 and will triple the operator's delivery capacity)5.

During 2020 and due to the health emergency, the concept of

shipping neutrality that is, the idea that logistics and shipping operators offer equal treatment to all e-commerce players, failed.

Many e-commerce players claimed to have received a worse service than that received by the big players. Of course, this reflects on the clients. They received packages from large e-stores to their doorstep on the chosen time and day and at a low cost, while the packages purchased from small stores were often late, with less efficient customer service and often at a higher delivery cost.

The measures adopted include:

- one-to-one partnership with smaller local logistics operators aiming for proximity and customisation. Tender is one example, which manages on demand logistics for boutiques and e-commerces in Milan, Florence, and Turin. These are tailored one-to-one deliveries: a “personal style rider” has zero impact and contactless delivery, with the possibility of immediate return and sanitation included. Another example of efficient partnership is UBM (Urban Bike Messenger) that runs last mile deliveries in Milan and Rome, with (professionals) bikers who can carry up to 100 kg per trip.

- assignment to local e-commerce platforms for the shipment management of products that otherwise would not have benefited from a digital platform. In 2020, delivery methods specific to each city were born: such as the Cerea online platform, which aims to deliver for shops in the Turin area, with local products, and with delivery within 24 hours of ordering; or Bergamo Smart Shopping, a home delivery service in the city of Bergamo, having the characteristics to challenge large marketplaces;

- third-party partners who interact for them, such as the choice of relying on logistics brokers who can negotiate the same treatment given to large e-commerce players for small operators and thus allow them to offer their consumers the same shipping and delivery standards;

- logistics hubs in the city, with small sorting spaces for last mile deliveries, also using shops and offices, closed due to health restrictions. Such as Dark Stores of big Fashion companies that transformed their shops into e-commerce warehouses.

It is easy to imagine how Italian e-commerce companies level of satisfaction regarding shipping services dropped significantly in 2020. In addition to having to find alternative solutions, some operators lost turnover due to logistics operators failing to manage the shipment during the peak of requests.

For these and other reasons, shipping services were rated satisfactory by only 25% of respondents (versus 44% last year); while the share of those thinking that the service can be improved is growing (65% of companies). The number of those thinking about changing provider because of unsatisfactory services increased (19%).

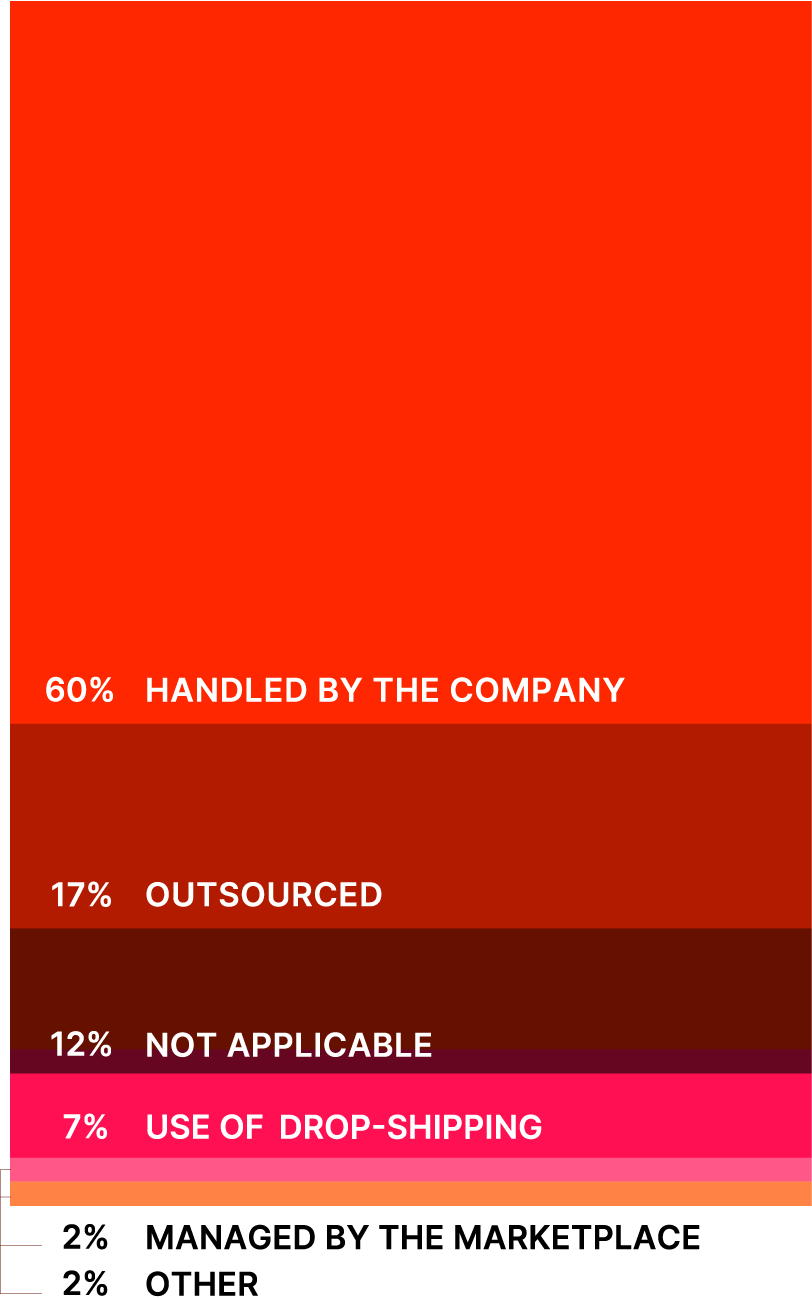

In addition to the above information, among the existing 2020 trends to solve problems related to shipping, there is the internalisation of the company’s warehouse task (for 60% of Italian e-commerce), which allows for greater control over stock and shipping, to the detriment of warehouse logistics managed by marketplaces (chosen by 2% of respondents, versus 9% in the previous year).

Some have built a winning strategy by using this method, such as the privately managed wine e-commerce Negozio Del vino, which grew a lot last year, and made logistics (managed internally by the company) one of its strengths, against its competitors: they have managed the difficulties of the Pandemic by offering a punctual and fast delivery service, recognised by the consumer.

Despite 33% of online purchases in 2020 being shipped using dropshipping (thanks to players such as Oberlo, BigBuy and Yakkyofy, some of the most relevant in Italy6), this solution decreased its appeal during the year among the e-commerce operators interviewed (for 7%).

17% of companies decided to rely on third-party partners for warehouse management and the choice of adopting alternative solutions to store goods gains a few percentage points, together with the share of those who do not need a warehouse because they sell digital products.

Also in Italy, shipments are adjusting to the trend of customisation, offering consumers a shopping experience increasingly linked to their needs and habits and aimed at strengthening their relationship. 49% of e-shoppers think it is important to choose the delivery time of their package and 60% think it is important to have more delivery places available to collect/receive their package

7. Amazon stepped up: in 2020, in addition to giving clients the possibility of having multiple delivery addresses and pick-up locations to choose from in their accounts, in Italy it also implemented the possibility of choosing the day and time slot for package delivery. There are six time slots during the day, every two hours (from 9:00 to 23:00) from Monday to Friday.

In the third quarter of last year, Zalando increased its turnover +21,6%8 thanks also to its new partnership with Poste Italiane which allows e-shoppers to collect and return packages at 12,000 authorised Italian post offices and through Punto Poste network (7,300 tobacconists, 200 affiliated shops and 350 lockers).

Another example is the shipping and price comparison platform Truckpooling, which grew by 50% last year, and which gives clients the possibility to customise the delivery: delivery to your floor, choice of pick-up and drop-off points, but above all insurance and the possibility of paying with “Borsino” (a deposit on the account, that can be topped-up and transfered)

9.

The acquisitions trend is also present in the logistics and shipping sector. Poste Italiane, for example, in 2020 has increased the customization of tIn 2020, Poste Italiane, for example, increased the customisation of the service by acquiring two leading startup in last mile delivery: Milkman and Sennder. These two companies supported the Italian operator in deliveries dedicated to the e-commerce (especially same-day deliveries) also in new sectors such as Food, and in improving GPS tracking systems to provide more accurate estimates to the customer.

Source:

1: Senza i big, emergono i piccoli, il Sole 24 ore, 2020;

2: I cambiamenti negli acquisti online, prima e dopo il lockdown: un’analisi sui dati dell’eCommerce, Qaplà, 2020;

3: Logistica e coronavirus: doccia gelata per il trasporto merci, ISPI, 2020;

4: e-Commerce in Italia, spedizioni in crescita del 30%, PMI, 2020;

5: Poste, l’e-commerce spinge la ripresa, Corriere, 2020;

6: Yakkyofy: velocizza e semplifica le vendite online, Startupitalia, 2020;

7: Si rafforza l’asse Zalando-Poste: in Italia 20mila punti ritiro, Corrierecomunicazioni, 2020;

8: Col coronavirus cresce il fatturato di Zalando, LaStampa, 2020;

9: Truckpooling, la start up delle spedizioni online, cresce del 50%. In arrivo nuovi corrieri e logistiche dedicate all’e-commerce, Radio Senise Centrale, 2020;

Download the complete research

DownloadThe 19th edition of the CA research will explore innovations, current trends, the most interesting cases and market evolutions of the Ecommerce in Italy.

More info

Discover moreDownload the report

DownloadDiscover data and trends on ecommerce in Italy and download our reports.

Researches Archive

Read moreCasaleggio Associati's ranking of The Best online Stores in Italy

Discover the interactive ranking

Discover more

Casaleggio Associati

Phone +39 02 89011466

VAT 04215320963

Contact us

Follow us on social:

©

© Casaleggio Associati 2025

All rights reserved.

We encourage sharing.